![How to govern [not like that]](https://substackcdn.com/image/fetch/$s_!emEQ!,w_80,h_80,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa9d7f587-4c16-42f0-9526-b00edc0ab4c8_155x155.png)

![How to govern [not like that]](https://substackcdn.com/image/fetch/$s_!Te2X!,e_trim:10:white/e_trim:10:transparent/h_72,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F51c6c618-ff5a-481b-b4e2-28047c606ca8_990x369.jpeg)

![How to govern [not like that]](https://substackcdn.com/image/fetch/$s_!emEQ!,w_36,h_36,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa9d7f587-4c16-42f0-9526-b00edc0ab4c8_155x155.png)

Forget ‘good’ corporate governance. What’s ‘good enough'?

What follows is the script of my “valedictory address” to the conference of the Global Research Foundation for Corporate Governance, which met at the London campus of Loughborough University, September 11-13, 2024. I welcome comments, either here or privately.

Since 2018, I have chaired the board of a major social care provider in England. I will soon complete my tenure as a non-executive director of a large performing arts organisation after quite a challenging six years. Covid brought existential threats to both organisations, and with it big – and aggressive – shifts in strategy for each. It was, in hindsight, a good time to be a company director; it might have been a very bad time. The difference was a combination of luck and very hard work. However, both cases bore only a passing resemblance to what we scholars talk about as “good” corporate governance. Yet both outcomes were undeniably good for the organisations and the people they serve. I’d like to speak about that today, but in terms of theory and as it pertains to boards of directors.

The purpose of this conference is an admirable one – to identify fruitful paths for future research in pursuit of the elusive goal of good corporate governance, not just in developed markets of the northern hemisphere but also those in what we (oddly?) call the Global South. I’d like to start with a bit of history, however – and more than a bit philosophy – so we can see better where we currently stand.

Let me warn you: My history lesson will be tendentious. I’ll say things I cannot demonstrate empirically and make assertions without solid evidence. That is, I will claim as true statements that are at best hunches that have coalesced into beliefs. They are really questions masquerading as statements.

And as you know – or should at least bear in mind – beliefs need constant attention. They need attention to the grounds on which they are based, and to the logic and theories – what epistemologists call the “warrants” – that connect the grounds to the claims (Toulmin, 2003). So, believe nothing of what you are about to hear. But if you hear something that sounds right or even possible, you may just have found something new to research.

What is corporate governance, anyway?

I’ve written two books and perhaps 50 articles with this term in the title or keywords. Since I retired nine months ago, I’ve blogged about it (at How to govern [not like that]),and about governance more generally – the governance of states and markets. Almost 30 years ago – well before I became a late-career academic – I started up a newsletter about it. Why? Because the directors I met, the newspapers I read, the public policy debates I participated in all talked about corporate governance. And – despite my 25 years in financial journalism – I didn’t have a clue what it meant. I even doubted whether the people writing and talking about it did either.

Corporate governance seems not to be a field at all. Is it finance or accounting? Management or leadership? Organisation studies or human resources management? Strategy or risk avoidance? Is it ethics, or just crime and punishment? It’s a landscape of many fields separated by rather fuzzy and permeable boundaries.[i]

For a long time, it didn’t even have a name.

Before the publication of the Cadbury Code in Britain in 1992, the term “corporate governance” was largely absent from our vocabulary – of commerce, financial markets, and even academia. People argued over some of its (many) themes much earlier, however.

For example, in 1932, Berle and Means (1932) wrote about the separation of ownership and control, a phenomenon that had worried Adam Smith (1776/1904) in his Wealth of Nations more than a century and a half earlier. You know this. But they never said: “corporate governance”.

The ‘industry’

Over those last 30-odd years, corporate governance has become an “industry”. This idea was an intellectual toddler in the 1970s, having sprouted from changes in the practices of financial markets. The poor profitability of conglomerate corporations, particularly in the United States, and the swelling paycheques of CEOs stimulated a wave of shareholder activism. Corporate raiders, we called them, and they broke up the behemoths. Mutual funds, the new kids on the investment block, clamoured for a voice on remuneration. Regulators responded by forcing companies to make more meaningful disclosures. Annual reports crept from 20 pages to 50, to 150 and more.[ii]

Academics quickly caught wind of the debate. Jensen and Meckling (1976) provided an economic argument for the shareholder side. Their article didn’t use the “G” word. But through it, and the work it inspired, the worries that Berle and Means and Adam Smith had expressed received a label – the agency problem (Fama & Jensen, 1983). But the language wasn’t yet of “corporate governance”, not for the public at least.

Institutional investors made an ethical argument against the executive stealing and shirking, one that seem to be based on the principle of justice as fairness as articulated by the political philosopher John Rawls (1971). Investors should have a strong voice in such matters, this argument goes. They bear the residual risk. After all, property rights are one of three bases of a just society, alongside life and liberty. So the great Enlightenment philosopher John Locke (1690/2005) taught us. Right?

But Rawls has his critics, particularly over the mythical “veil of ignorance” he employs over those who set the rules of the game. And Locke has his, not least over what “property” means – think of slavery – and whether it requires the centrality he ascribed to it in the rule-making and governance of states.

In corporate governance, investors were engaged not in ethics but in what we might call an exercise in corporate politics, conducted via the corporate ballot box, a contest against entrenched managements for control over the resources of the company. Those political battles led to new rules – in academic language new institutional arrangements – created by markets and regulators alike. They changed the rules of the corporate governance game.

The contestation sounds like one about principles; but let me – controversially, and for the sake of argument – advance an alternative reality. It was also a power grab. Institutional investors, for their own greedy purposes, used trick after trick to seize greater control over corporate resources. It wasn’t a moral crusade. Had it been such, private, retail shareholders would have been direct beneficiaries, rather than the power residing with the big fund managers. And as big fund managers morphed into either giants or specialised boutiques, they further disenfranchised retail investors. Then they elbowed pension funds into the background, then even the ultra-high-net-worth families. Retail wealth management became fund-of-fund management. Stock-picking went out the window. Instead, the (we) little folks pick which fund managers they’ll (we’ll) follow. The investment supply chain grew longer, with each link grabbing another bit of the surpluses that companies themselves managed to produce (Kay, 2012).

This disenfranchisement was endorsed in the Cadbury Code itself, a new form of governance that became a model for the rest of the world. Institutional investors would be responsible for policing the code. They were given a “power of arrest” for executive pay. Within boardrooms, their representatives – the “non-executive” directors – would keep the executives under regular surveillance, so the managers of these giant funds and boutiques could concentrate on reeling in the savings of retail investors, pension funds and ultra-high-net-worth families, thus consolidating the giants’ own power. Sometimes they failed at the task. I’ll name-check: Bernie Madoff, as in “made off with your money”.

A nascent alternative, proposed and discarded decades earlier, was revived as a counter-revolution, initially by trade unions and the socialist end of the national political spectrum. They called it corporate social responsibility (CSR). It was, again, an appeal to ethics – an appeal concerning corporate duties and stakeholder rights. Their claims included, among other things, that alongside shareholders, workers bear residual risk. Labour contracts are at best incomplete. Workers make a psychological investment in the companies they work for, investing social and intellectual capital (Gleeson-White, 2020).

But as we’ve seen with first wave of corporate governance, CSR quickly became a battle for power, most centrally to do with workers wresting some degree of control from both management and investors.

You’ve probably read about “managerial discretion” (Finkelstein & Hambrick, 1990; Hambrick & Finkelstein, 1987), the freedom of managers to act, or the constraints on them. Boards constrain managers, shareholders constrain boards, stakeholders try to muscle their way in.

Now we have ESG – the environmental, social and governance movement – which makes a claim as a new ethical view of how corporations should be governed. The E and S sound a lot like elements of CSR. But the G is the key. The focus on G in the investment community is a way to reassert investors’ claim for primacy. To paraphrase George Orwell in Animal Farm: “all stakeholders are equal, but shareholders are more equal.”

From these part-ethical and tangibly political waves, new institutional arrangements followed. Law, regulation, and where they didn’t work, codes of corporate governance proliferated, grew longer, creating an ever-expanding list of principles and provisions with each iteration.

During the past 30-odd years, these waves of concern about corporate governance have had some benefits. Boards of directors work harder now, to be sure. But executive pay continues to climb, some say exponentially. Even more importantly, corporate collapses were not banished; indeed, they have grown more damaging. The Global Financial Crisis of 2007-09 had a much greater impact than anything since the Great Depression in the 1930s, even worse than the time of Enron, WorldCom, Parmalat, and all the others in 2001-03 (Nordberg, 2020b).

Climate-related concerns have a much greater profile now. But unlike the wave of CSR and the workforces that backed it, the climate lacks an obvious constituency in corporate politics, and investors watch constantly in which direction the political winds are blowing.

Witness how Larry Fink and BlackRock have backtracked, last year and this, on the climate-change agenda they had set for themselves in 2019. G trumps S and E. Especially in Trump-leaning America. And if there ever was a need for ethical deliberation, it is climate change. Climate, signified by the E in ESG, struggles, still, to gain traction in the political debate that follows ethical decision-making. Climate action has, as yet, evaded institutionalisation. Or rather: institutionalisation has bypassed climate.

What about the future?

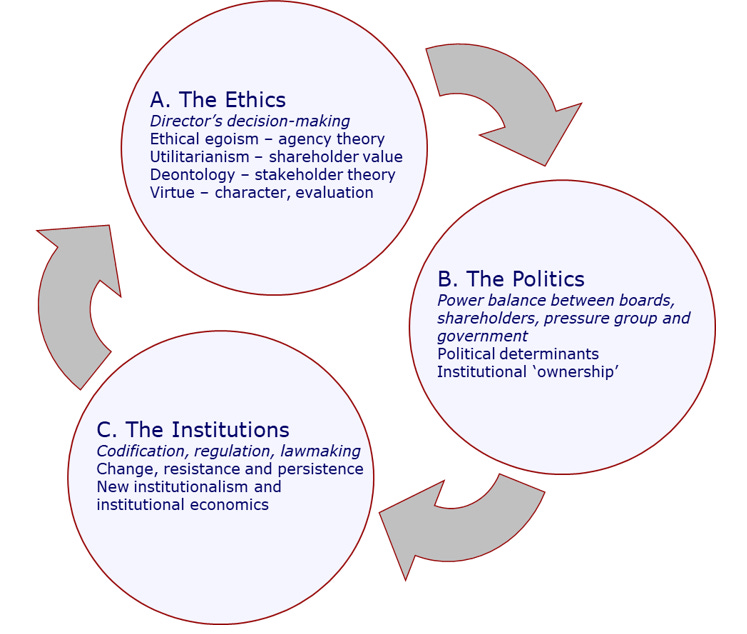

You’ve heard my interpretation of the past. Ethics – politics – institutions. The paper I presented in an open session this morning considered an aspect of the ethics of corporate governance. My contribution to yesterday's panel looked at the politics. This talk concerns institutions and their benefits, but it focuses on the drawbacks.

Institutionalisation lets everyone off the hook. We don’t have to think anymore. We just follow the rules. Academic research finds new ways to add new “mechanisms”, each striving for an elusive goal: good or even “best” governance. We think an independently minded board is a good board. A majority of directors should therefore be independent non-executives. Our research articulates definitions of independence. Term limits. Gender quotas. Racial quotas. Committee structures. Financial expertise. Board size – that’s a Goldilocks constraint, not too large, not too small, in academic speak, an inverted U relationship. They all seek precisely the same goal: to make sure the board thinks before it acts. In academia, we call that “board effectiveness”. Do we need to follow all those “rules” to achieve independent thinking? Each “mechanism” makes corporate governance, well, more mechanical. Better rules, or just more of them?

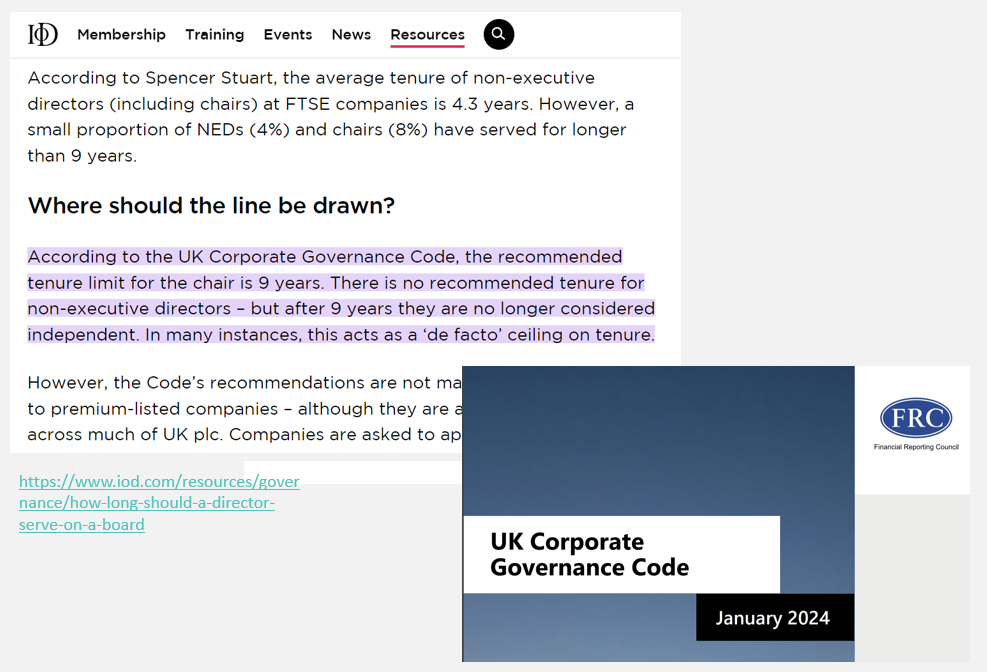

Let me give you an example: A few years ago, I interviewed the chairman of a large, listed company, a FTSE250 firm. He opened our conversation by telling me – with pride – that he had just persuaded one of the non-executive directors to stand down after serving eight and a half years. That meant the company wouldn’t run afoul of what he called, and what a lot of other people still call, the code’s “nine-year rule”. It’s meant to ensure directors do not get too close management. It isn’t a rule, just a recommendation, subject like the rest of the code to “comply or explain”. But the governance rating agencies and proxy voting firms treat it like a rule. So do many of the asset management firms that subscribe to those services, and who vote on whether the chairman and other directors should be re-elected to the board. So, the chairman had dodged a bullet.

However, that wasn’t the end of his story. The chairman then told me that this non-exec was the hardest working of all his directors. Not only that, that director had detailed, field-level knowledge of an important aspect of the business. He was a lawyer, too, an American, resident and practicing law in the United States. And the company was facing a major lawsuit, in the States, on precisely that aspect of the company’s business.

Had the chairman really dodged the bullet? More like shot himself in the foot.

Viewed from a company’s position in this landscape of corporate governance, the layers of rules – of institutional arrangements, erected by states, markets, and the corporate governance “industry” – constrain their freedom to experiment: with financing, with strategy, and even with the governance arrangements, let alone with their products and markets.

Moreover, many of the “mechanisms” of corporate governance – and much of our research – follow similar logics. They tell directors what to do. They don’t show them how to think.

So, perhaps we scholars should forget achieving “good”, let alone “best” practice in corporate governance. What might this landscape look like if we strive instead for governance that’s “good enough”?

That, I think, is where we researchers – you, mainly; I’m a practitioner now – could add some tangible value.

Let’s look at institutions

Thirty-two years ago, the Cadbury Code set off a wave of reforms across the Global North and South. Over time, the code added layer-upon-layer of controls, many of which tried to do the same things. And it’s not just formal codes. Look at the data that governance ratings agencies collect and analyse, the sort of stuff academic researchers often use to measure the dimensions of good governance.

Consider this: The leading provider, ISS, lists 230 factors that go into its Governance Quality Score calculation. Any individual company can expect to be ranked on 120 of them. They create a further set of rules that a company will follow – or violate at its peril. These are the private sector equivalents of regulation. They have become embedded in practice – in a word, institutionalised, but in the sociological sense of being taken for granted. We often hear that doing the same thing over and over and expecting a different outcome is the definition of madness. Like the corporate governance madness of 2007-09.

These observations demand that we address a series of research questions:

If the goal is “best practice”, let’s study at the micro level: What mechanisms work well in combination with what other mechanisms?

A lot of the mechanisms of corporate governance strive to achieve the same goal: greater accountability of management to shareholders.

(a) Which ones are redundant? Is it enough to have three rather than seven – or 120 – for each problem area?

(b) Which combinations work well, and in which circumstances? And why?

Where should we set the boundaries between law, regulation, codes, and the ratings police?

The preamble to the 2010 UK Corporate Governance Code – written personally by Sir Christopher Hogg, who chaired the Financial Reporting Council – declared that the “code is not a rigid set of rules”. It was a heartfelt plea, he told me in during a two-hour interview. Among his many accomplishments,[iii] Sir Christopher had been CEO of a FTSE100 company. He had chaired another, my old employer, Reuters Group plc, for 19 years. He worried about where corporate governance was headed. His comments helped me to see that the analyses of ratings agencies may well work at portfolio level, helping the buy-sell-hold decisions of asset managers, but make a mess of the practice of any individual company.

So, what experiences have individual companies had in defying the tyranny of ratings and codes? What experiments have been successful?

In conclusion …

At the outset, I promised a philosophical and challenging talk, fitting for a conference that strives to present a global view of the many fields that make up the landscape of corporate governance. My talk today has focused just one country – Britain – so its lessons may be limited. But limited in what way? Practically? Ontologically? Epistemologically?

First, and related to practice, the UK Corporate Governance Code has been a model that countries around the world, north and south, have used.

Second, and ontologically, that is evidence that leads us to think there’s something universal in it, or at least that there is something universal about human nature, about the laws of economics. But corporate governance, at a national level, is also subject to local laws and regulations, local customs and practices that are taken for granted, in short, local institutional arrangements, adding layers to the combinations of “mechanisms” that the corporate governance industry has imposed on practice.

This is an area ripe for research, though – epistemologically – with a lot of uncertainty whether we can find the “truth”.

Then there are industry norms – industrial standards, contracts, supply chains, etc. – that the globalisation, or better, the semi-globalisation of commerce (Ghemawat, 2003) has brought into play. These too are institutions, and institutions enable certain actions and constrain others. These need to be considered when a company’s board decides what sort of governance is most appropriate to its circumstances. These themes too deserve more and subtler research.

Governing the corporation is more than all these layers of institutional arrangements, however. It involves dealing with the politics of governance, the play for power over corporate resources and decisions. It involves, too, the people behind the decisions, and whether they decide in a mechanical way, or instead in an ethical, thoughtful way (Nordberg, 2023). We researchers would do well to be thoughtful, particular, granular, and sensitive to the complexity of the phenomena we set out to research, including their contextual and historical contingency.

Plato thought there was an ideal form of governance (1974). However, idealism has been beaten into retreat in modern and postmodern philosophy. The complexity we see suggests that even thoughtful corporate governance won’t eliminate mistakes. Decisions will be experiments, that is; and they should be. Some will work. Other won’t. That’s the lesson – on ontological, epistemological, and ethical levels – of the philosophy known as pragmatism (James, 1907/1955).

I speak to you now as a practitioner, a respondent to codes, regulations, law; as a user of academic research; as someone who engages in the political contest over resources; and as someone who is trying to what’s best for the people whom my two boards are entrusted to serve. I can assure you: Formal compliance is not the same thing as doing a good job.

As Professor Terry McNulty and I observed about a decade ago:

“Codes of corporate governance may identify structures, define independence and allude to key relationships, but they can only take a board so far along the path to effectiveness. In the end, it’s a local matter” (Nordberg & McNulty, 2013, p. 367, emphasis added).

Let’s forget about achieving good governance. Forget about discovering what the elusive best governance might be. Let’s find out what sorts of governance – plural – are good enough (Nordberg, 2018, 2020a).

Berle, A. A., Jr., & Means, G. C. (1932). The Modern Corporation and Private Property. New York: Macmillan.

Fama, E. F., & Jensen, M. C. (1983). Agency Problems and Residual Claims. Journal of Law and Economics, 26(2), 327-349. doi:10.1086/467038

Finkelstein, S., & Hambrick, D. C. (1990). Top-Management-Team Tenure and Organizational Outcomes: The Moderating Role of Managerial Discretion. Administrative Science Quarterly, 35(3), 484-503.

Ghemawat, P. (2003). Semiglobalization and International Business Strategy. Journal of International Business Studies, 34(2), 138-152. doi:10.1057/palgrave.jibs.8400013

Gleeson-White, J. (2020). Six Capitals: Capitalism, Climate Change and the Accounting Revolution That Can Save the Planet (Updated ed.). Sydney: Allen & Unwin.

Hambrick, D. C., & Finkelstein, S. (1987). Managerial Discretion: A bridge between polar views of organizations. In L. L. Cummings & B. M. Staw (Eds.), Research in Organizational Behavior. Greenwich, CT: JAI Press.

James, W. (1907/1955). Pragmatism: A New Name For Some Old Ways of Thinking – Popular Lectures On Philosophy. New York: Meridian Books.

Jensen, M. C., & Meckling, W. H. (1976). Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. The Journal of Financial Economics, 3(4), 305-360. doi:10.1016/0304-405X(76)90026-X

Kay, J. (2012, July). The Kay review of UK equity markets and long-term decision making - Final report. Consultation of the UK Department of Business, Innovation and Skills. Retrieved from http://www.bis.gov.uk/assets/biscore/business-law/docs/k/12-917-kay-review-of-equity-markets-final-report.pdf

Locke, J. (1690/2005). Second Treatise on Government. Project Gutenberg. Retrieved from http://www.gutenberg.org/ebooks/7370

Nordberg, D. (2018). Edging toward ‘reasonably’ good corporate governance. Philosophy of Management, 17(3), 353-371. doi:10.1007/s40926-017-0083-9

Nordberg, D. (2020a). Media Review: Daniel S. Milo, Good Enough: The Tolerance of Mediocrity in Nature and Society. Organization Studies, 41(6), 899-901. doi:10.1177/0170840619871177 or https://eprints.bournemouth.ac.uk/32595/7/Nordberg%20BookReview%20GoodEnough%20OS%20jul19.pdf

Nordberg, D. (2020b). The Cadbury Code and Recurrent Crisis: A Model for Corporate Governance? Cham, Switzerland: Palgrave Macmillan.

Nordberg, D. (2023). A pragmatist case for thoughtfulness and experimentation in corporate governance. In T. Talaulicar (Ed.), Research Handbook on Corporate Governance and Ethics (pp. 310-327). Cheltenham, Glos.: Edward Elgar.

Nordberg, D., & McNulty, T. (2013). Creating better boards through codification: Possibilities and limitations in UK corporate governance, 1992-2010. Business History, 55(3), 348-374. doi:10.1080/00076791.2012.712964

Plato. (1974). The Republic (D. Lee, Trans. 2nd ed.). Harmondsworth, England: Penguin.

Rawls, J. (1971). A Theory of Justice. Cambridge, MA: Harvard University Press.

Smith, A. (1776/1904). The Wealth of Nations. In. Retrieved from http://www.econlib.org/library/Smith/smWNCover.html

Toulmin, S. (2003). The Uses of Argument (Updated ed.). Cambridge: Cambridge University Press.

[i] Spoiler alert: I still don’t know what it means. Perhaps words don’t have meanings: People have meanings, which they attach to the words they speak or hear. A word, as Humpty Dumpty told Alice in Through the Looking Glass, “means just what I choose it to mean – neither more nor less.”

[ii] ExxonMobil’s 2023 annual report was 152 pages, including lots of pictures; its picture-less 10-K filing to the SEC was 172 pages, more than 60,000 words. BP plc’s 2023 Annual report and 20-F SEC filing, words and pictures, took up 392 pages.

[iii] Christopher Hogg had advised Sir Adrian Cadbury about the code in 1992 and much later headed the UK Financial Reporting Council, which oversees the code.