![How to govern [not like that]](https://substackcdn.com/image/fetch/$s_!emEQ!,w_80,h_80,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa9d7f587-4c16-42f0-9526-b00edc0ab4c8_155x155.png)

![How to govern [not like that]](https://substackcdn.com/image/fetch/$s_!Te2X!,e_trim:10:white/e_trim:10:transparent/h_72,c_limit,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F51c6c618-ff5a-481b-b4e2-28047c606ca8_990x369.jpeg)

![How to govern [not like that]](https://substackcdn.com/image/fetch/$s_!emEQ!,w_36,h_36,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa9d7f587-4c16-42f0-9526-b00edc0ab4c8_155x155.png)

Day of jackals – Is the corporate governance pendulum swinging back to managers?

Two news stories, either side of the Atlantic, seem to flag the possibility that the institutional investors may be losing their hold on power over the corporations in which they invest.

In the United States, Charles Elson, founding director of the Weinberg Center for Corporate Governance at the University of Delaware, raised an alarm bell when the state legislature passed a bill to change corporate law. Delaware is important because about half the companies based in America have their legal seats in that state. Writing in the Financial Times, Elson said the bill “would lead, in effect, to the self-destruction of its [the state’s] corporate role — with serious consequences for investors worldwide”. The change is one of three that clarify ambiguities in recent Chancery Court decisions. The Council of Institutional Investors has urged the governor to veto the bill. [At the time I’m writing this piece, the bill is awaiting the signature of the governor.]

In Britain, the Financial Conduct Authority (FCA) decided to change substantially the listing rules for the first time in more than 30 years. It’s been under discussion – undergone two public consultations – but the outcome is nonetheless even more significant than what many expected.

In the US, Delaware’s move met controversy. The Delaware public radio station summarised it this way:

The bill has garnered significant opposition from the legal community in Delaware and across the country, including the top judge of the state’s powerful Chancery Court. Under the proposal, a Delaware company could make a side agreement with a single shareholder without a full vote of the board of directors.

All investors are equal, but favourite investors are more equal.

In Britain, the new rules make it easier for founders of companies to maintain control when they list on the London Stock Exchange. That much had been expected. But the final rules, coming into force on July 29, mean that their venture capital backers and other early holders can also outvote the new institutional investors.

All investors are equal, but early investors are more equal.

The FCA’s move overturns three decades in which listing rules frowned on any companies that violated the “one share, one vote” principle. Those three decades also correspond to the time since the Cadbury Code, and the regular revisions to what is now the UK Corporate Governance Code, called on mainstream investors to play the role of enforcing governance standards (Nordberg, 2020).

The effect of both developments seems likely to give corporate managers greater say over strategic decisions and relegate the supposed watchdogs of governance to a side show.

The FCA described its move this way:

The overhaul of listing rules better aligns the UK’s regime with international market standards. It also ensures investors will have the information they need to make decisions about their money, while maintaining appropriate investor protections to hold the management of the companies they co-own to account.

The new rules remove the need for votes on significant or related party transactions and offer flexibility around enhanced voting rights. Shareholder approval for key events, like reverse takeovers and decisions to take the company’s shares off an exchange, is still required.

That is, disclosure will have to suffice because voting power will rest with those who build the business, rather than those asked to finance its future growth.

I’m not taking sides in either dispute. When I started paying attention to such matters, 40-odd years ago, both Delaware and Britain were manager-friendly legal regimes. Then things changed: In the US, executive pay disputes and weak financial performance, particularly for conglomerates. In Britain, the collapse of several large companies in the late 1980s and early 1990s. Did the pendulum then swing too far?

For the British action, there are benefits that come with letting the people who took the early risk continue to benefit from it as firms continue to innovate that grow. If the new investors see their role as passively benefiting from a share price rise while actively monitoring and controlling management, “one share, one vote” brings a heavy risk. And the US market has long tolerated preferential voting, and it’s one of the reasons British companies have been undervalued and why some have abandoned the London Stock Exchange to list in New York or on Nasdaq.

What worries me is how you break through that structure when it ceases to bring the benefits, when the founders lose their mojo, the venture capital funds want to bail out and got somewhere with more mojo and without the monitors and controllers looking over their shoulders.

For the Delaware action, there’s a bigger issue. What corporate governance scholars and company law experts call “related party transactions” present a serious issue. They may have benefits, of course, but they are also channels for draining corporate resources for the benefit of some. It was this problem that led to the famous case of Parmalat, Italy’s contribution to the global crisis in corporate governance in 2003.

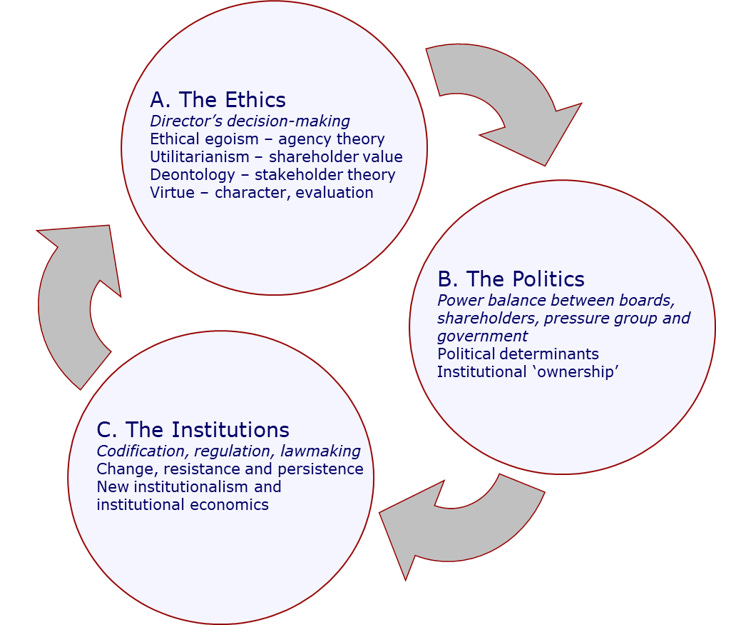

Some issues in corporate governance involve ethical decisions, but the decisions themselves set off politicking between shareholders, boards and other parties, which are in essence disputes of power (Nordberg, 2009; 2010). They resolve themselves in new institutional arrangements, which then take the place of ethics in decision-making. You just follow the rules. But in the current cases, the rules are changing in response to the power plays of various actors who may dress up their arguments in terms of utilitarian ethics when they are properly ones of who benefits, and not why they should benefit, and not others.

Nordberg, D. (2009). Politics in corporate governance: How power shapes the board's agenda. Retrieved from http://ssrn.com/abstract=1332310

Nordberg, D. (2010). The Politics of Shareholder Activism. In H. K. Baker & R. Anderson (Eds.), Corporate Governance: A Synthesis of Theory, Research, and Practice (pp. 409-425). New York: John Wiley & Sons.

Nordberg, D. (2020). The Cadbury Code and Recurrent Crisis: A Model for Corporate Governance? Cham, Switzerland: Palgrave Macmillan.